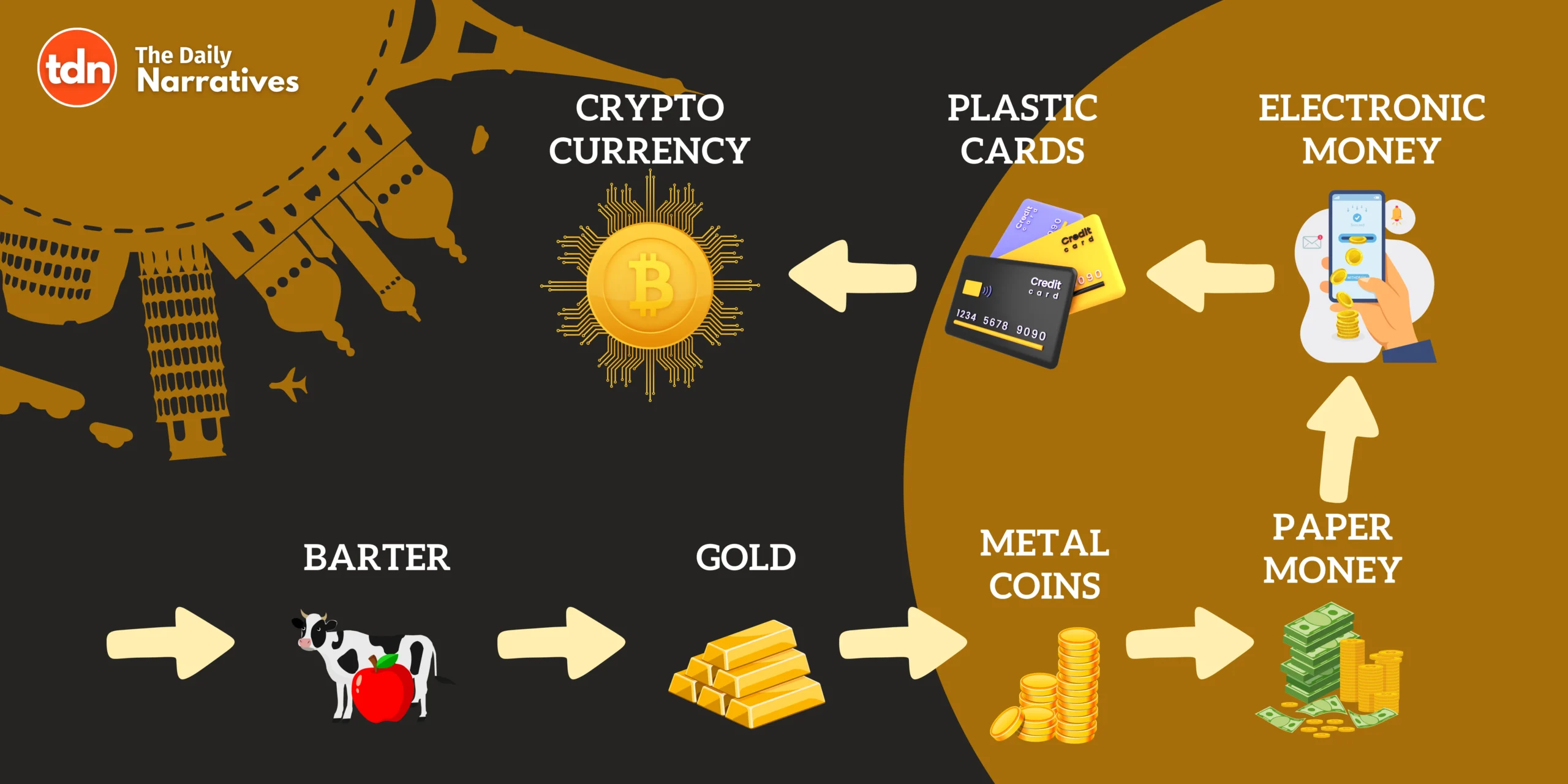

Long ago, people didn’t use money like we do today. Imagine living in a time when if you wanted something, you had to swap something you had for it. This was called the barter system. So, if you had extra apples and wanted oranges, you had to find someone who had oranges and wanted apples. Sounds simple, but it was pretty tricky because the person you found had to want exactly what you were offering, and you had to agree on how much one thing was worth compared to the other. Plus, imagine trying to split a cow into two to trade it for other things – not really practical, right?

Because bartering was so complicated, people started looking for better ways to trade. This search led to the creation of what we now call money. The first official coins were made over 2,000 years ago! Then, about 800 years ago, gold coins became popular in Europe. Fast forward to the 1600s to 1900s, and paper money became the way to go, used by people all around the world.

Today, we have lots of ways to pay for things. We use cash, coins, credit cards, and even digital wallets on our phones like Apple Pay or PayPal. But all these ways are controlled by banks and governments. They decide how money can be used and keep track of it all.

Enter cryptocurrency – the newest form of money. Unlike the other types, no single group or person controls it. It’s all digital, which means you can’t hold a Bitcoin in your hand like you can with a dollar bill or a coin. But you can use it to buy things or trade it, just like any other money. Cryptocurrency works using a technology called blockchain, which keeps it safe and lets people make direct trades with each other, anywhere in the world, without needing a bank to check everything.

So, from swapping apples for oranges to tapping your phone to pay, the way we use money has changed a lot! Cryptocurrency is just the latest step in this journey, making it easier for everyone to trade and buy things in a whole new way.

{kind=link}